Consider this graph, comparing the Administration’s forecast to the latest WSJ forecast, and the error-correction model that includes the population forecast.

Figure 1: Reported GDP (bold black), Administration forecast (red squares), WSJ April poll means (blue), error correction model with GDP-population vector covariance (dark blue), +/- 1 standard error band (light gray lines). Source: BEA, WSJ April survey, author’s calculations.

The Administration’s (pre-war) forecast is much higher than the WSJ’s forecast (and Stanley’s top forecast at Santander US Capital Markets*). It is also higher than the forecast I make using (pre-War) data on GDP and population plus one standard error. (See comparisons in this post).

My error correction model assumes that the GDP-population relationship to 2028Q1 is the same as it was for 1996-2025. The Department of Management asserts that labor productivity growth will increase at a faster rate. From the Economic Report of the President, 2026 (Chapter 9):

Labor productivity growth (measured as output per hour in the non-farm sector) is expected to be 2.9 percent over the 11-year projection period, much faster than the 2.1 percent annual growth rate during the years 1953-2019 (table 14-5, row 5, columns 1 and 6). Labor productivity is expected to be boosted by Administration policies, such as deregulation (see chapter 2 of this Report) and the OBBBA tax policy that promotes growth leading to an increase in income per worker. In addition, the increasing use of artificial intelligence is widely expected to boost product growth. The United States has experienced long-term labor productivity growth at that pace before, most recently during the 15-year period 1948-63.

In Chapter 2, which recounts the benefits of deregulation under the Trump Administration, the Report notes (p.62):

To reverse these [Biden era] regulations—assuming their costs directly reduce GDP without reducing market benefits—could increase annual US GDP growth by 0.29–0.78 percent over the next two decades.

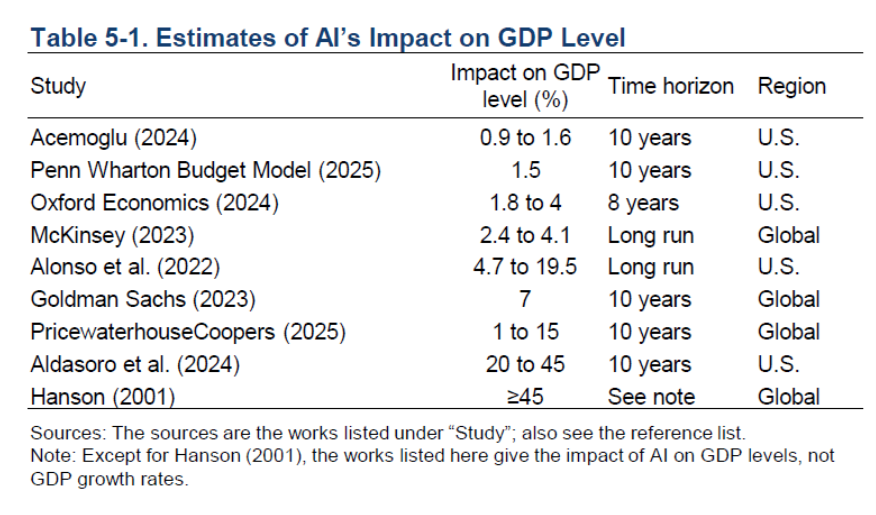

Regarding AI-based productivity growth, Chapter 5 of the Report includes this table:

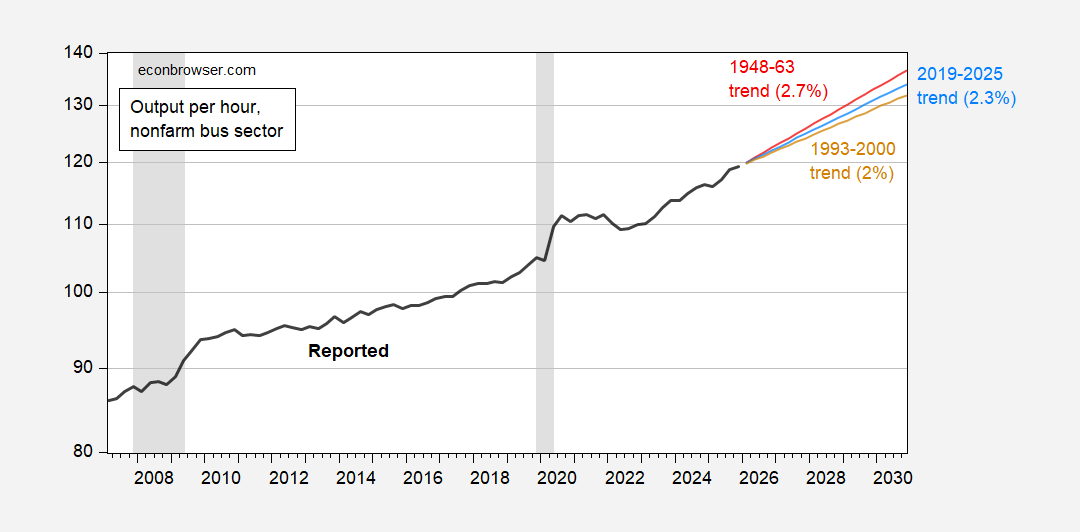

Indeed, labor productivity has increased rapidly in recent years. For comparison, I plot hourly non-farm business output, the Administration-accepted trend (stochastic), the 2019-25 trend, and the 1993-2000 trend (proxy for the dot.com productivity boom).

Figure 2: Hourly nonfarm business sector output (bold black), Administration’s 1948-63 trend (red), 2019-2025 trend (light blue), 1993-2000 trend (light brown), all on a log scale. The NBER has defined recession days as shaded in gray. Source: BEA, NBER, and author’s calculations.

Growth rates are calculated as log differences (which is why the 1948-63 growth rate differs from the 2.9% reported in ERP).

It will be interesting to see how CBO considers the President’s budget, given the difference in growth and tax revenue, in these two (almost simultaneous) projections.