We had a record low in U.Michigan consumer sentiment in May (prel.). Given that the actual compounding exits are rising smartly (see this post), why is sentiment so low? Have there been structural disturbances?

Figure 1: The poverty index is equal to the sum of unemployment and the annual inflation rate, % (black, left scale), the U.Michigan Consumer Sentiment index inverse (teal, right scale). The NBER has defined recession days as shaded in gray. Source: BLS, U.Michigan via FRED, NBER, and author’s statistics.

A quick look suggests a break starting in 2022, with the relationship between the U.Michigan sentiment index skewed in different directions and the Misery Index.

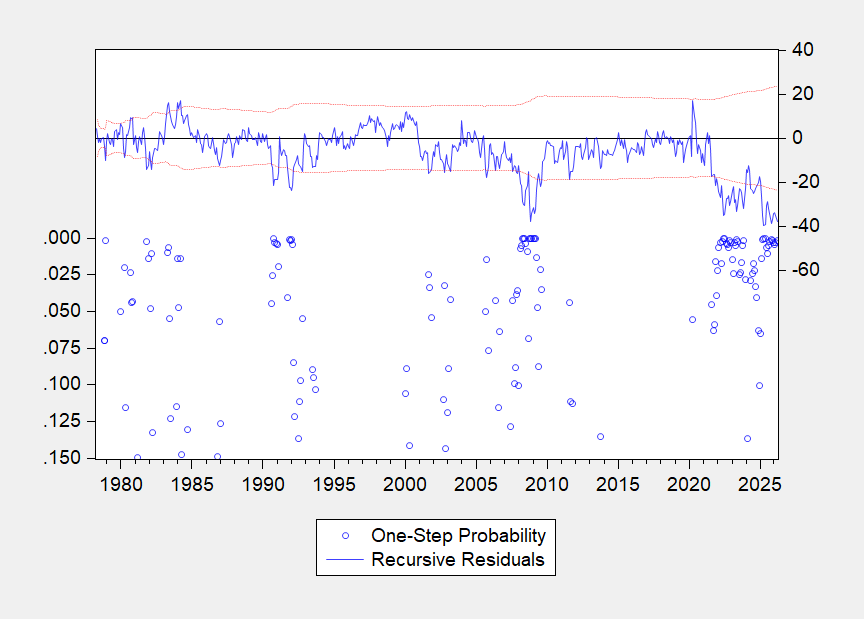

To test this formally, I estimated a linear regression between the U.Michigan index and unemployment and inflation entered separately; adjusted R2 is 0.25. Using the one-step Chow prediction test for the break, I get the following:

Figure 2: One step forward is the prediction Chow test.

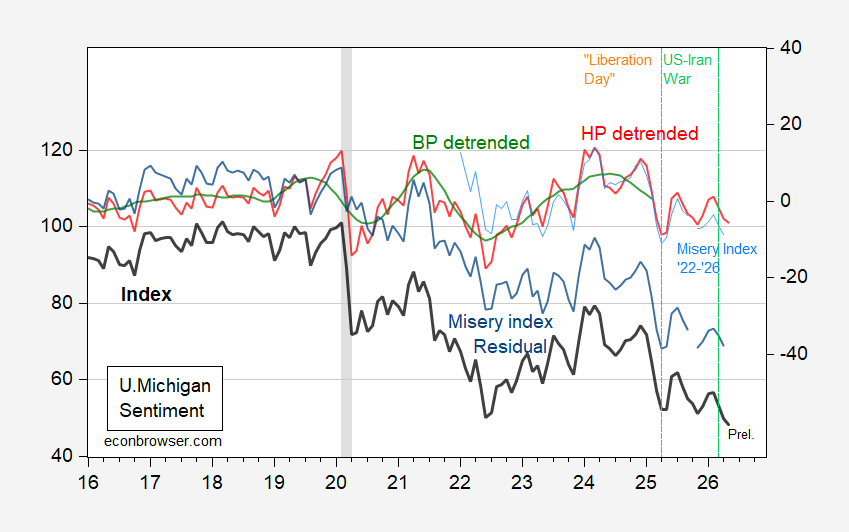

One might say one of the structural breaks was in 2022, but to let the data speak, I applied a battery of filters to the data: Hodrick-Prescott and Band-Pass (Baxter-King). In addition, I have omitted the use of unemployment and inflation over the entire period 1978-2026, as well as the shorter period 2022-2026. The results are shown in Figure 3, along with the U.Michigan green sentiment index.

Figure 3: U.Michigan sentiment (bold black, left scale), HP detrended (red, right scale), Band Pass filter, two components (green, right scale), misery index residual (blue, right scale), and misery index regression 2022-26 residual (blue, right scale). The NBER has defined recession days as shaded in gray. Source: U.Michigan via FRED, NBER and author’s statistics.

On the other hand, HP detrended sentiment does not look very low in May. All of this means that there is a new mathematical “norm” for emotions. From a more economic perspective, the results clearly show that in recent years, sentiment has been lower than predicted by official unemployment and inflation, from the “Misery index residual”. Cutting the sample period to 2022-26 (the assumed inflationary period) results in a smaller surplus.

The obvious question is what explains the divergence between unemployment and inflation on the one hand, and sentiment on the other. Here we have an embarrassment of riches. It may be highly sensitive to inflation. For example, inflation doubled in value in the period 2016-26. Therefore, the heavy weight of inflation after decades of inflation is evident.

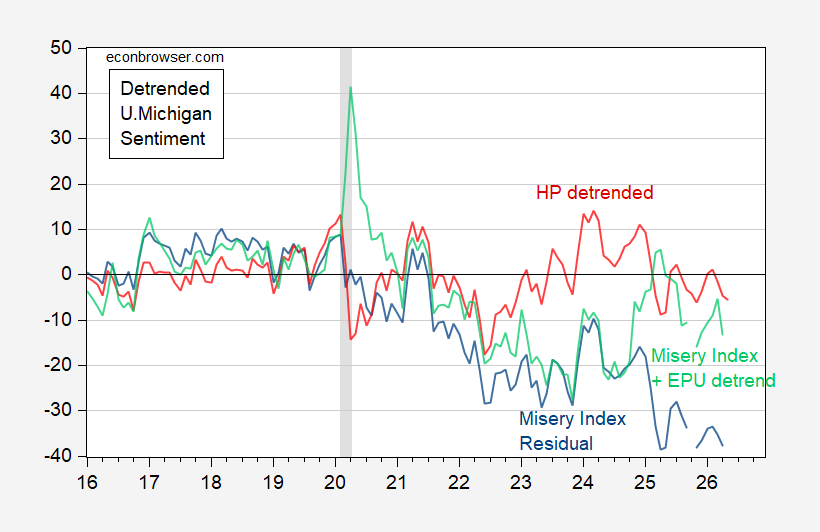

Increasing economic policy uncertainty is another possibility. Including the Baker-Bloom-Davis EPU doubles the adjusted R2 over the period 1985-26, for example. The large gap between predicted and actual emotion then disappears. This result is shown in Figure 4.

Figure 4: HP detrended centimet (red), distress index residual decline (blue), and distress index and EPU residual decline (light green). The NBER has defined recession days as shaded in gray. Source: U.Michigan via FRED, NBER and author’s statistics.

Another possibility is the fact that employment and inflation are felt more unevenly, more than ever, and this is reflected in the decline in historical correlation.