Guest Contribution: “Does the Productivity Curve Still Predict Recessions? Evidence from the US and the OECD”

Today, we are pleased to present a guest contribution of Dear Chen (University of Wisconsin).

An inverted yield curve is often seen as an early warning sign of a recession. A large body of research suggests that the yield curve helps predict both growth and decline in GDP, particularly in the United States and Europe. Recent experience, however, has raised doubts about how reliable that signal remains. In mid-2022, the yield curve inverted again in the United States and several major OECD economies, yet no recession followed. That has led many observers to question whether the yield curve still has the predictive power it once did.

In this post, I revisit that question by examining how the yield curve predicts recessions in the United States and seven OECD countries. I also test whether adding the debt service ratio improves the performance of the forecast, as suggested by Borio, Drehmann, Xia (2018). I find that forecast accuracy is improving in five of the eight countries tested, suggesting that debt burdens may help buffer the risk of recession. These international differences raise questions about the channels through which the debt service ratio affects macroeconomic risk. Overall, the findings suggest that the yield curve still contains useful information, especially when combined with debt burden measures.

I use monthly data on yield spreads, recession indicators, short-term interest rates, and debt service ratios for the United States and seven OECD countries from 1995 to 2025. The yield spread is defined as the difference between the 10-year interest rate and the 3-month interest rate. Interest rate data comes from the OECD and FRED, debt service ratio data from the BIS, and recession indicators from the NBER and the Economic Cycle Research Institute. I estimate probit models through 2021 to predict recessions over the next 12 months and examine the out-of-sample forecasts from 2022 to early 2026 using the Brier score.

The figures below show the yield curve and recession periods for each country.

The relationship between the yield curve and recession is not the same across countries. In the sample, not all recessions were preceded by an inverted yield curve. At the same time, every country except Japan experienced an inversion of the yield curve by 2022, even if that inversion did not lead to a consistent recession. If this apparent relationship is not consistent across countries, the next question is whether a simple predictive model can still extract useful predictive information from it.

I estimate and compare three probit models for each country: one uses the yield spread alone, one adds the short-term interest rate, and one adds the debt service ratio. Each model predicts the probability of a recession in the next 12 months based on current financial conditions. The yield spread captures expectations about future economic activity, while the debt service ratio reflects the debt burden faced by households and firms and can help capture financial risks missed by the yield curve alone.

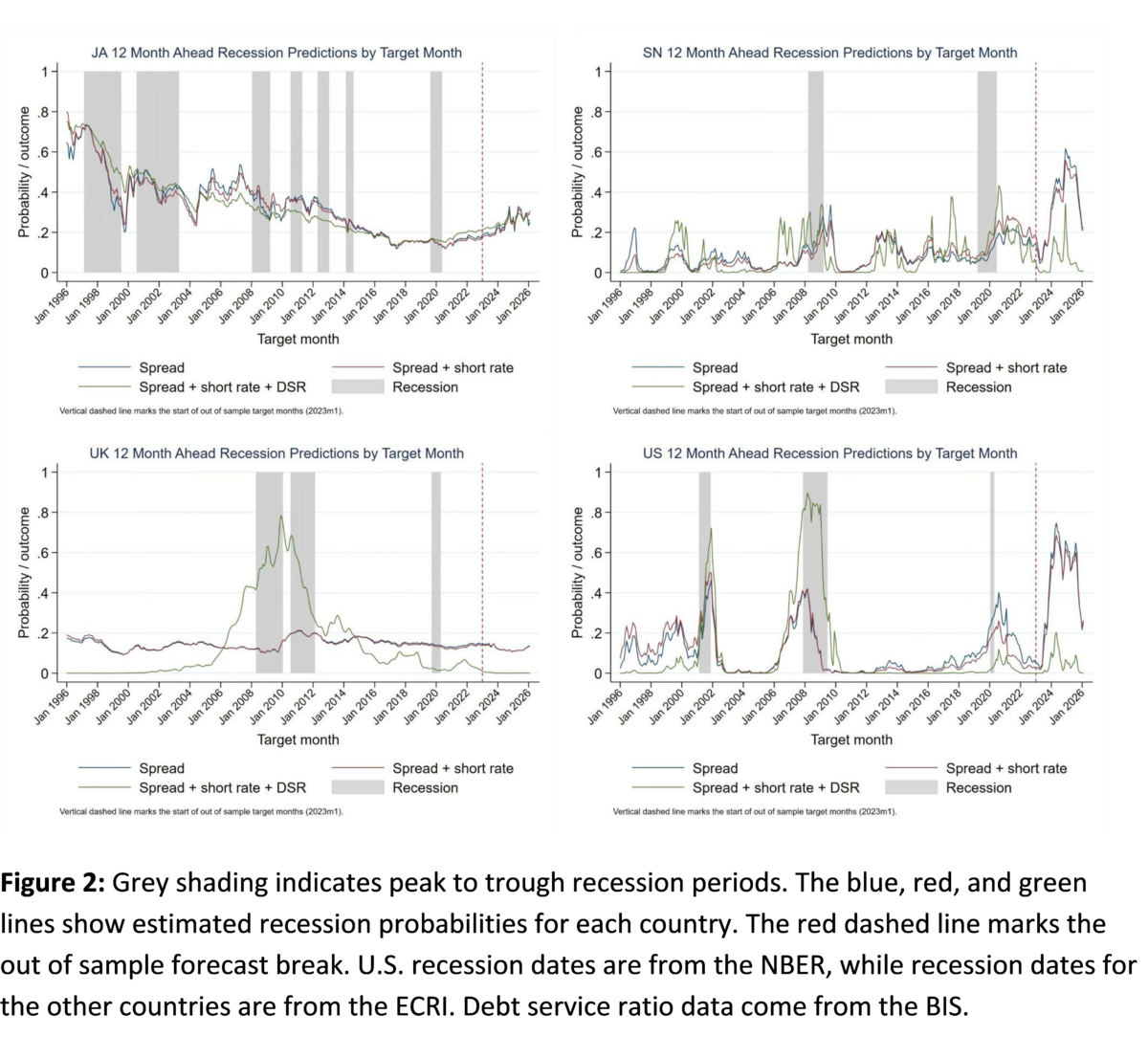

The figures below show the 12-month forecasted recession probabilities and recession times for each country in the target month.

Statistics suggest that the yield curve still contains useful information about recession risk, especially before 2022. In many countries, the predicted probability of recession increases during recessions, suggesting that the pattern is not random. Still, models don’t always push that probability above 0.5, a common threshold for predicting a recession.

Adding the DSR also significantly changes the probabilities of recession predicted over the period 2023–25 in some countries. This is especially clear in the United States, where both the distribution-only and short-term + models predict a high probability of recession in 2024. A similar pattern is seen in Sweden. In the United Kingdom and Italy, adding DSR apparently reduces the predicted probability of recession, although the original models do not exceed the 0.5 threshold for predicting recession. In contrast, the benefits are less clear in Canada, France and Germany. In Canada and France, the observed differences across specifications are less pronounced, while in Germany adding DSR significantly raises the predicted recession probability.

These results should be interpreted in accordance with the recession time convention used here. The analysis relies on recession days defined by NBER and ECRI, which are converted to 1/0 recession indices. However, underlying economic conditions are continuous rather than binary, and the designation of a recession is often determined retrospectively using a variety of indicators rather than a single rule of thumb. Therefore, forecasted probabilities deviate from the actual effects of a recession that may capture economic weakness or the risk of a recession that may not have developed into, or may not have been classified as, an official recession. This warning applies especially to countries where industrial production or manufacturing activity has weakened during the study period without being defined as a recession.

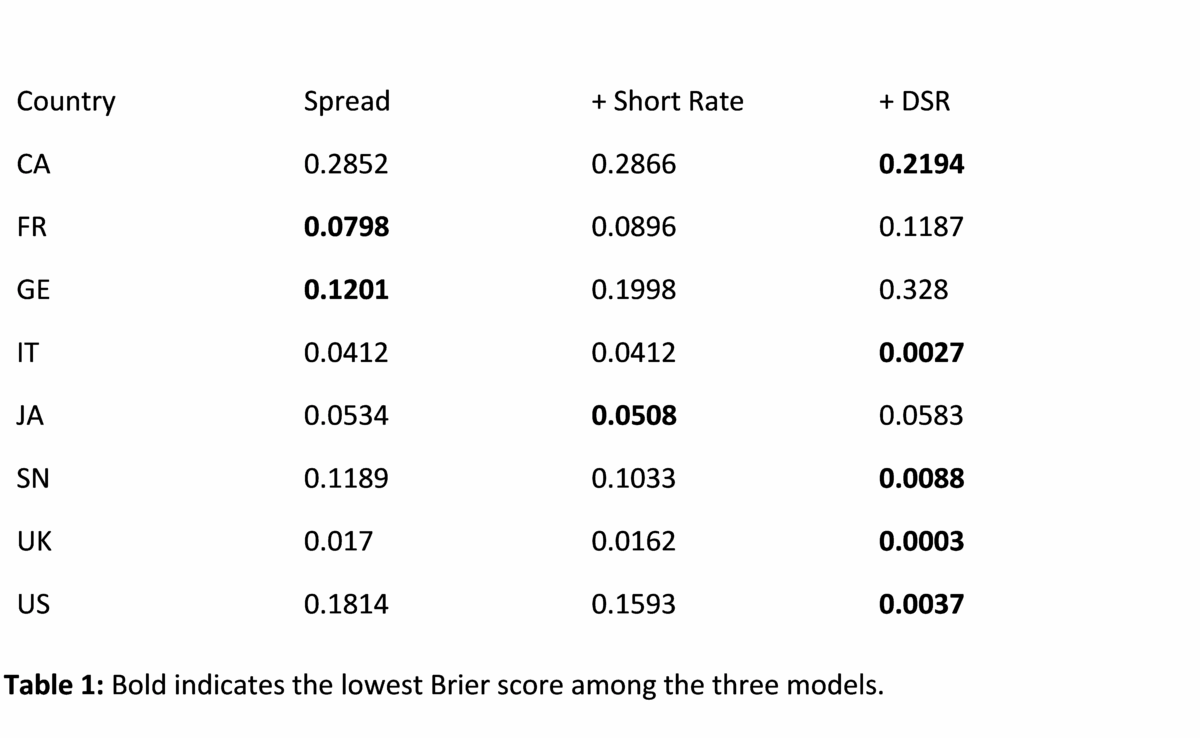

To formally test whether adding a debt service ratio improves forecast performance, I compare models using the Brier score, a measure of the mean squared difference between predicted probabilities and actual outcomes.

Table 1 compares the three models using the Brier score, where lower values indicate better forecast accuracy. For reference, a model that assigns a recession probability of 0.5 will always produce a Brier score of 0.25. This represents a 50-50 neutral prediction, so a Brier score of less than 0.25 suggests that the model’s predicted probabilities contain useful information beyond the naive benchmark. The best Brier scores in Table 1 are generally below that benchmark.

Adding the debt service ratio improves the performance of five of the eight countries in this sample: Canada, Italy, Sweden, the United Kingdom, and the United States. However, the pattern is not the same, as weather accuracy worsens in France, Germany, and Japan when the debt service ratio is added. These differences suggest that the role of debt burdens in predicting recessions varies significantly across countries.

Overall, the yield curve remains a useful predictor of recession risk, but its performance appears to be less robust than in earlier periods. Adding the debt service ratio improves forecast accuracy in several countries, particularly the United Kingdom and the United States. Taken together, these results suggest that debt burdens can provide additional useful information for predicting recessions, but that their value depends on the macroeconomic conditions of a particular country. Understanding the mechanisms underlying these international differences remains an important question for future research.

This post was written by Dear Chen.