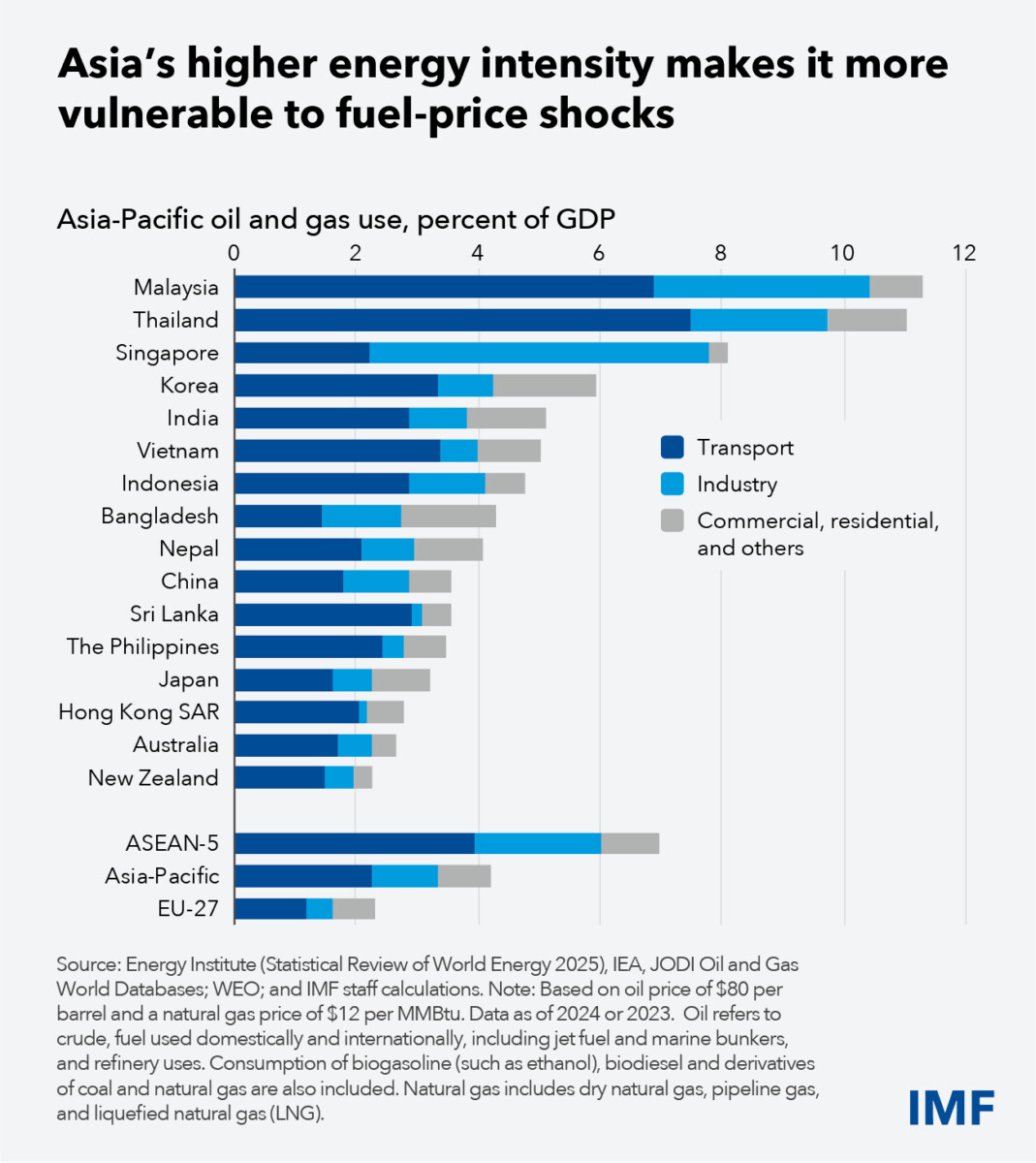

From the IMF’s Asia Pacific Department, the blog “Asian Economic Stability Tested by Energy Shocks”, two interesting tables: Dependence on oil and natural gas imports and energy.

First, oil and gas imports as a share of GDP, ranked from high to low. Singapore, Thailand, and Korea are the leaders, but India and Japan are not far behind.

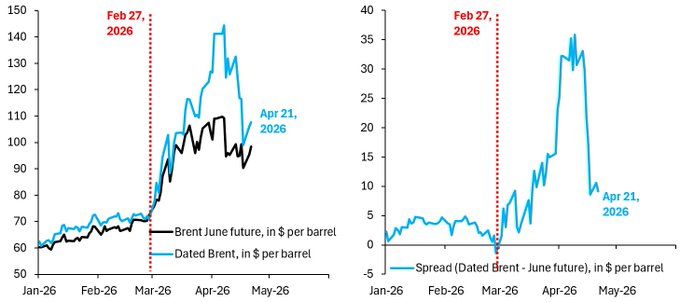

With Brent averaging $94/bbl in March, compared to $71 in February, a 32% increase. Brent inn April to 4/20 averaged $118/bbl, a 66.8% increase compared to pre-war. As long as the crude prices are not too far behind the currency prices, then in Korea, the transfer of spending power to the oil exporters will amount to 2.7 ppts of GDP (4 ppts x 0.67 = 2.7 ppts of GDP), assuming that the price does not change and there is no depreciation. Obviously, that’s an unsustainable assumption, in a year’s time, especially in the ever-evolving economy.

Now, even if the country had no oil imports, it would still be affected by high oil prices. That’s because oil prices are set on the global market, and so is the domestic price again International oil exports will increase. The impact on the general price level will depend on the share of oil consumption in GDP.

Therefore, a country like the US – even with a limited oil trade – will still experience a cost shock. In general, oil and gas dependence is about 4% in Asia-Pacific, almost double that of Europe. Therefore, the cost-push shock – which holds everything else – should be much greater than in Europe or North America.

Note that high price pressure can be reduced by subsidizing fuel, etc. However, this will impose significant financial costs (and delays in adjusting high rates)

Much as a difference has been made between physical and paper oil prices (futures), especially in relation to Asia, which relies heavily on oil from the Strait of Hormuz. That means some countries may soon face real shortages of crude oil and its derivatives. Such an event can have a qualitatively different effect from just high values.

Can we look at the spread between the Brent date as well June Brent as a deficit indicator? I’m not sure, although Robin Brooks points out that the spread has decreased in recent days.

Given that oil cannot move quickly, and many refineries in East Asia are designed to refine Gulf oil, it seems to me that a real shortage is indeed possible; AJOT – from the point of view of logistics – is consistent with this view (as Krugman). Robin Brooks on the other hand asserts that futures accurately reflect market conditions, which are set in an imminent doldrums/no rise scenario.

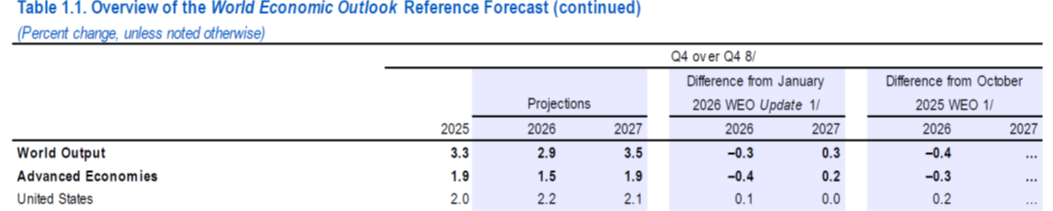

The IMF projects a 1% drop in growth compared to the baseline in the “adverse” scenario. This situation is described in the April WEO (page 7) as follows:

In the worst case, (1) Oil prices are assumed to increase by 80 percent from the second half of 2026 compared to the January 2026 WEO renewal baseline, before returning to about 20 percent above the baseline in 2027, with an increase in extinction in 2028 (corresponding to a price of approximately $0 in 2026 and approximately $75 in 2027). Gas prices rose in Europe and Asia by 160 percent in the second quarter compared to the baseline, before being revised further in 2027, and food prices rose by 2.5 percent. (2) Expected one-year pre-inflation rises by 50 basis points in 2027 in advanced economies and 90 basis points in emerging markets excluding China. Inflation expectations are unchanged in China, as current inflation makes this less risky than in other countries. (3) The de-risking episode increases corporate premiums in advanced economies and China by 50 basis points, while emerging markets excluding China receive a 100 basis point increase and a 50 basis point increase in sovereign spreads. The stabilization of financial conditions disappears in 2027. Given the large impact on inflation expectations, the monetary policy response gives less weight to output tightening than is often assumed.

What are the IMF WEO forecasts (q4/q4 growth) under the reference scenario:

Note that the US forecast for 2026 is faster relative to the January 2026 (pre-war) forecast, while China(Japan) moves by 0.6(0.5) ppts in 2026, and Emerging and Developing Asia as a whole moves by 0.3 ppts. For the “negative” scenario, remove the percentage of Emerging and Developing Asia…

See Cave in the NYT for more discussion of the potential implications.

I think most macroeconomists are too optimistic about the effects of war on the US economy, given the windfalls from AI investments. However, as an open-minded economist, I wonder how much of the outflow from the world’s most affected areas will force a review of America’s resilience. The US does not export much to East Asia, but we do export to countries that export to East Asia…