Using Today’s Futures, Don’t Expect Gasoline Prices to Return to Antebellum Levels Anytime*

Front month Brent futures (for June) jumped tonight. Where fuel prices are going, conditional on those coming days is anyone’s guess.

Figure 1: Brent oil price (black), NYMEX futures as of 4/19 (red), all in $/bbl. April view of data through 4/10. The NBER has defined recession days as shaded in gray. Source: EIA via FRED, NBER, barchart.com.

Using the log regression of the first difference of fuel prices on current and extreme oil prices for 1990M10-2026M03 (adj-R2 = 0.56), here is the conditional forecast of fuel prices:

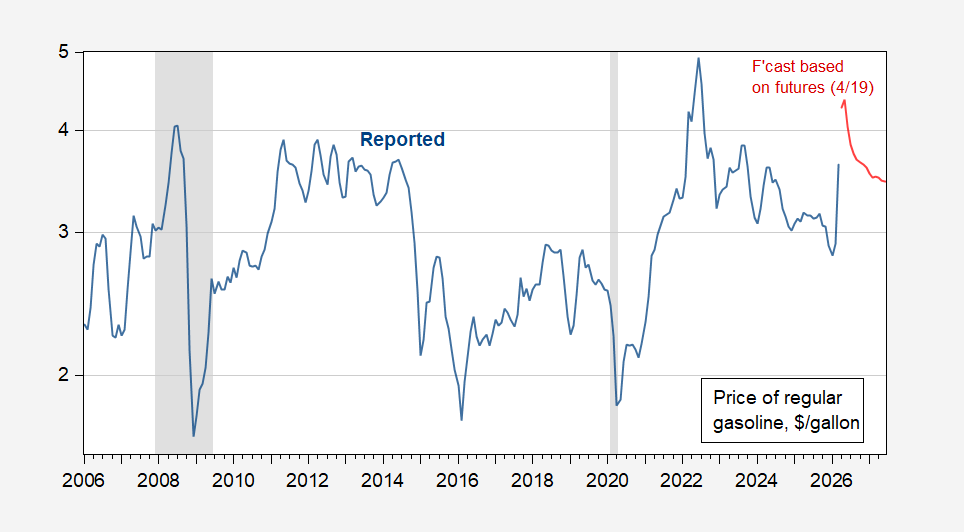

Figure 2: Standard gasoline price (blue), and forecast based on Brent futures (red), both $/gallon. NBER described the highest recession days in gray, barchart.com, NBER, and author’s figures.

Oil futures are relatively accurate forecasts, as discussed in Chinn and Coibion (2014). However, these tests tend to focus more on quiet time sampling periods. The future was not particularly realistic during the Iraq war of 1990-91, or the 2003 war, as noted in this post.

In the context of the current conflict, Norland (2026) notes:

…If the conflict ends soon and supply disruptions are resolved quickly, crude prices may go down a curve that leads to losses for anyone long. That said, the fact that the returns for holding long positions during contango periods tend to be negative, while the returns for holding long positions during pullbacks tend to be positive tells us two things:

Traders tend to underestimate how long an overinvestment period lasts. Therefore contango markets tend to stay at depressed prices for longer than investors originally thought.

Likewise, traders have historically tended to underestimate how long deficits last. This can be true for demand shocks, such as the rapid increase in demand from China and other emerging markets between 2003 and 2011, and it can be true for periods of supply disruption, such as following the US invasion of Iraq.

and:

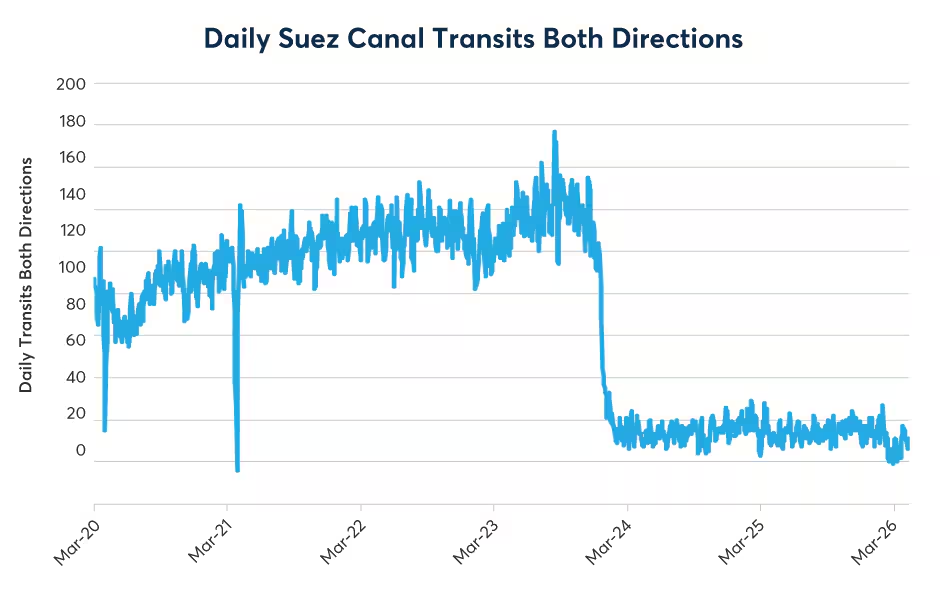

One important indicator to watch is traffic through the Strait of Hormuz (Figure 7). Also, what happened to shipping through the Red Sea and the Suez Canal provides a warning about how disruptions in supply can last longer than initially anticipated. After Suez traffic dropped in late 2023, it never recovered in part because insurance companies withdrew from the market (Figure 8).

…

In other words, even with the “reopening” of the Strait, actual oil prices may exceed the stated prices in the future.

A final reason to expect higher gasoline prices in the future, even if oil prices decrease: the asymmetric response of gasoline prices to oil prices. Gasoline prices increase rapidly with oil price increases, and decrease slowly with oil price decreases. This asymmetric response is called the “rocket and feather” thesis. For a review, see Wen et al. (2025). I ignored this effect in my regression specification above.

* Unless there is a global recession, which causes a significant drop in demand…