Central Banking news account from the ECB and Its Audience conference, Wednesday:

Bank of Finland Governor Olli Rehn, UBS chief economist Tao Wang and economics professor Menzie Chinn discussed the changing global environment. The governor of the Bank of Finland is focused on Europe, which in his opinion will face “asymmetric” consequences from the war in the Middle East because of its power dependence. Wang said China’s massive deterrence would protect it from the effects of conflict. Chinn said the credibility of the big banks will be tested next year as they deal with the crisis.

The conference agenda is here.

In my presentation, while enumerating the commonly discussed points about the various sensitivities and vulnerabilities of various key economies, I also made some exceptions. de facto the preferences and reliability of major banks are related. By de facto voting, I mean voting under pressure (government tweets, illegal prosecutions, etc.).

Regarding central bank credibility in an era of unprecedented presidential pressure, I noted the Bordo-Siklos measure of monetary credibility:

Figure 1: The Bordo-Siklos ratio of the Fed’s credibility in the low money market (blue). The calculation assumes the CPI target corresponding to the PCE target is 2.45%. Light orange shading denotes the Trump administration. The dashed orange line is “Independence Day”. The NBER has defined recession days as shaded in gray. Source: BLS, NBER, author’s statistics.

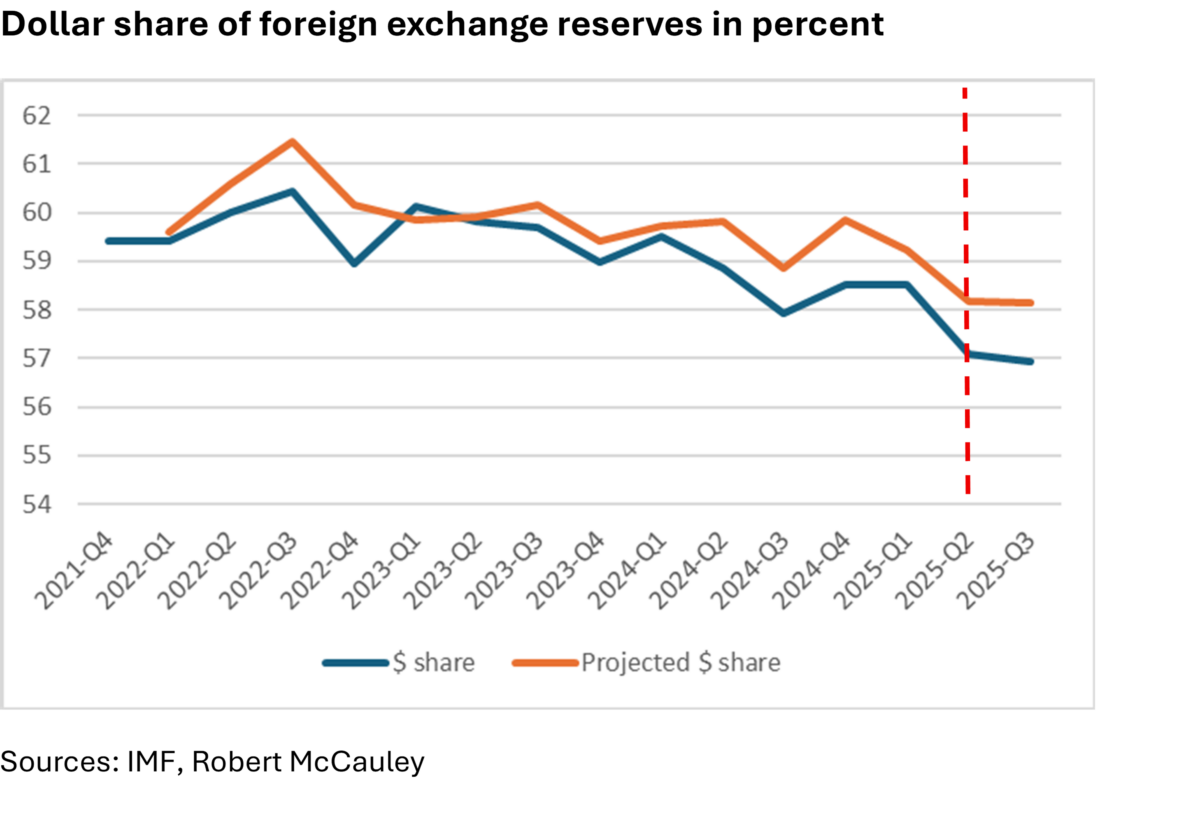

And in terms of the dollar’s role as the main international currency, this graph (just suggestive):

Source: McCauley (2026). The red dashed line is “Independence Day”. The expected dividend adjusts for price changes (eg, exchange rate changes).

Although this last graph is not evidence that recent administrative actions have reduced the role of the dollar as the main international currency, there is more evidence of an empirical nature about the impact of costs on central bank dollar reserves in Chinn, Frankel and Ito (2026). We do not have data for 2025 on individual central bank reserves (let alone 2024); but in the data up to 2023, we know that central banks in countries subject to Section 232 charges appear to increase their holdings of other currencies, and decrease their holdings of the US dollar. (I presented these results to the ECB on Tuesday; slides here).

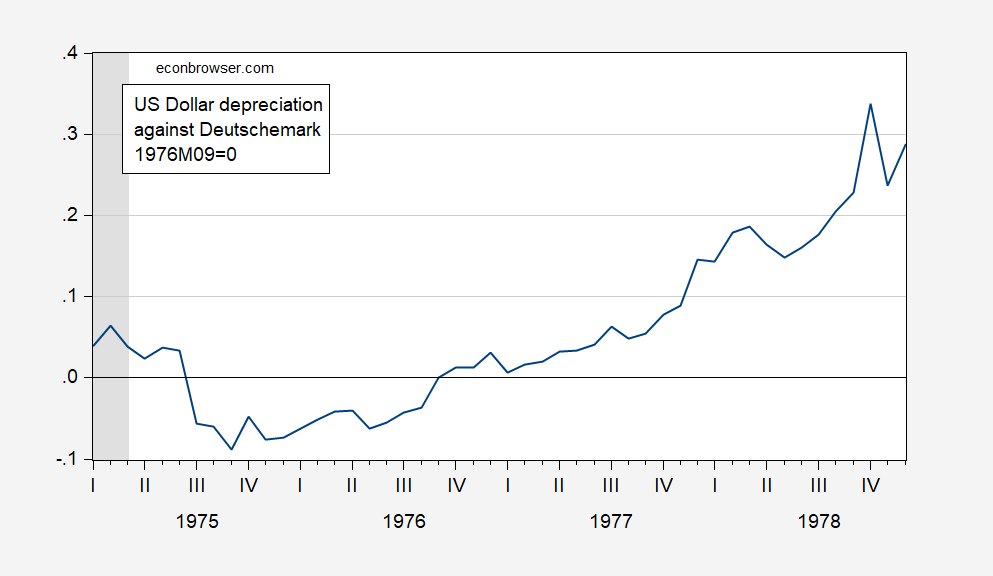

Let’s say Trump manages to put enough pressure on the Fed – either through verbal attacks, intimidation of mediators, prosecutions, or by sidelining current FOMC members in favor of unwelcome applicants – then monetary policy on this side of the Atlantic may become simultaneously less credible and more loose (on top of incredibly loose policy). In an environment with decreasing reliability, it may not be too big to see something like what was seen in the 1970s.

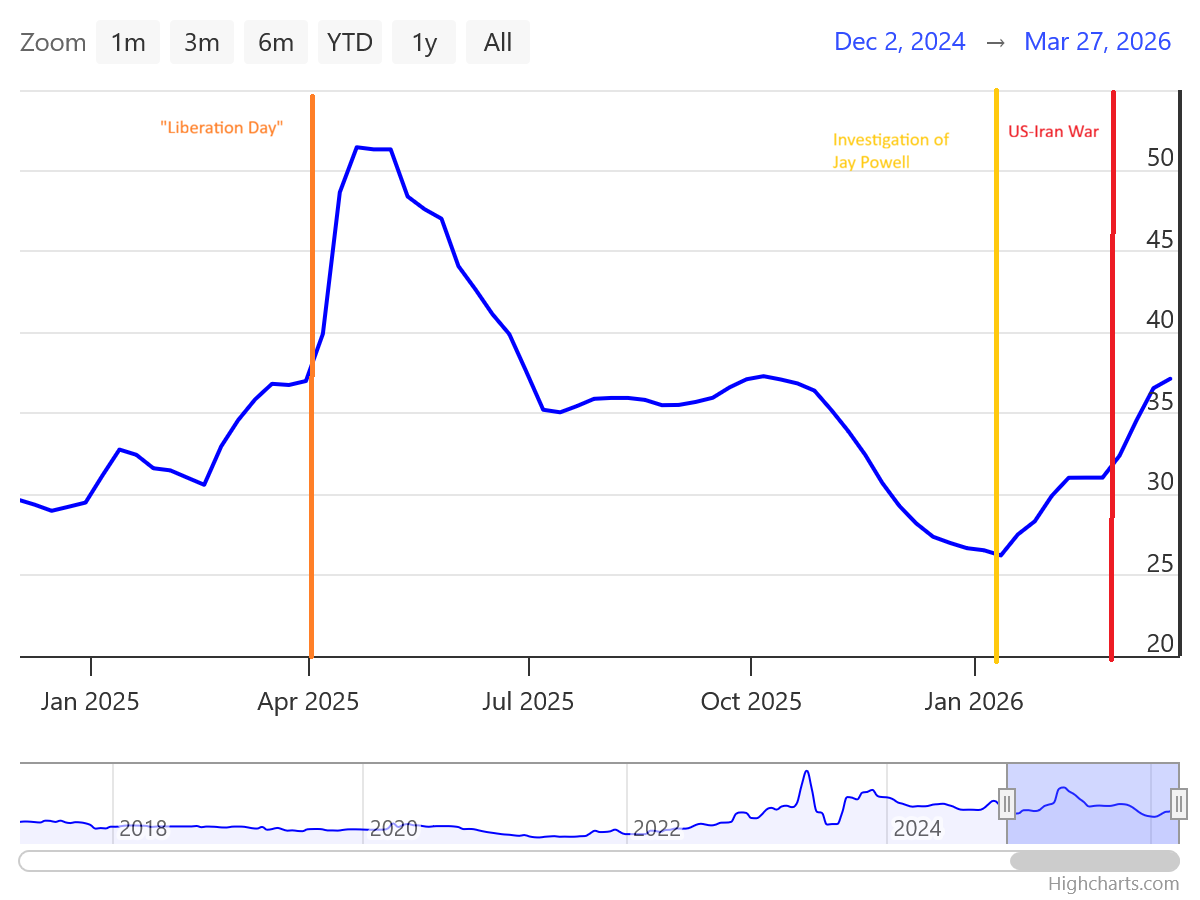

Could it be that the dollar is losing some of its qualities as a safe haven currency? I doubt we’ll see a big change, but the erosion could be slow. Five-year CDS prices suggest some results from the actions that management has taken.

Source: worldgovernmentbonds.com, accessed 3/27/2026.