Debt issuance increases, official foreign Treasury holdings decrease, the Fed reduces holdings, and expected inflation increases. How well do we predict prices?

First, the debt picture, and the 5-year debt projection according to the CBO:

Figure 1: Debt to GDP (black) and expected debt to GDP over the next 5 years under current law (tan). Source: CBO, January or February Budget and Economic Outlook stories, and author statistics.

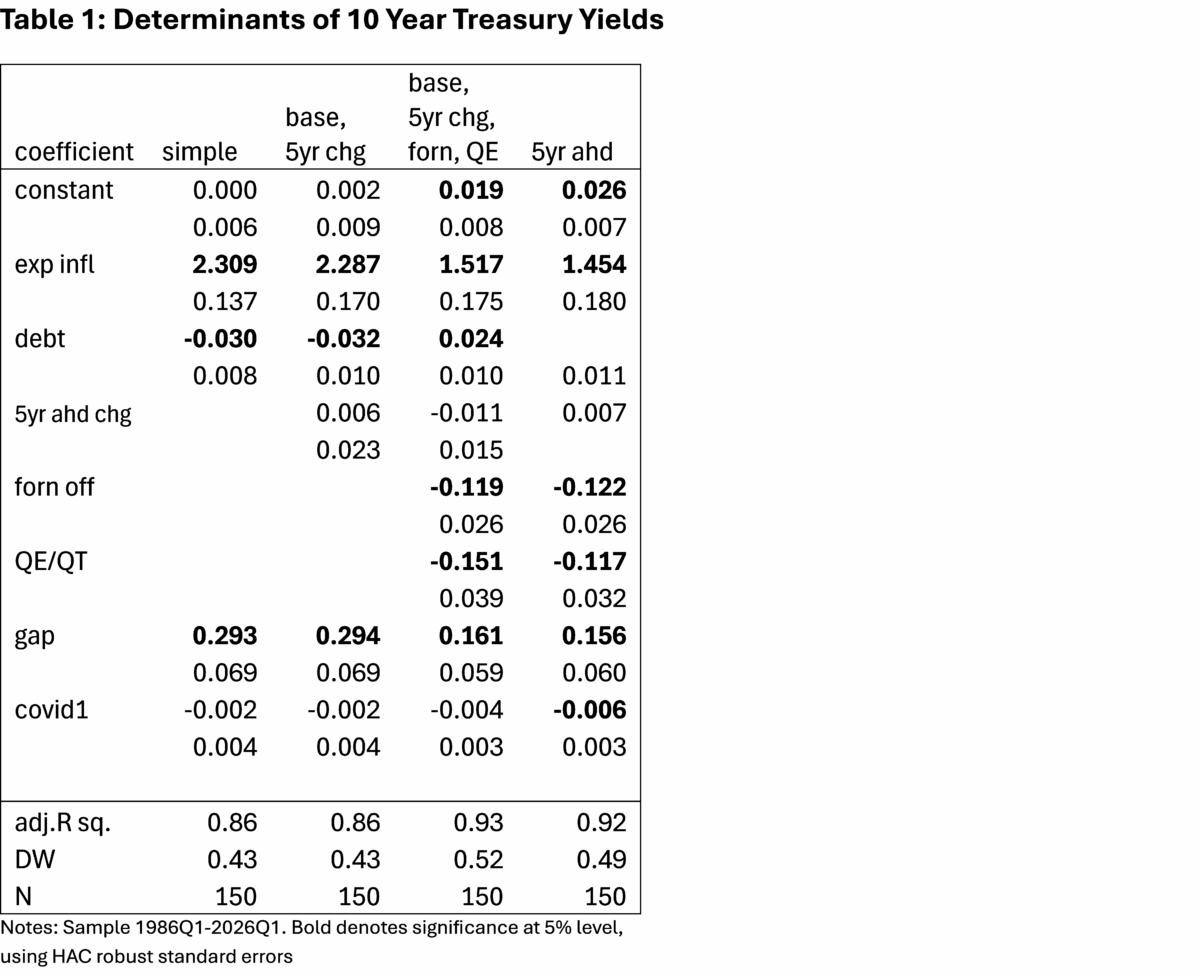

A simple correlation of debt to GDP and the value of the Treasury (normative or real) will show an inverse (negative) correlation (column 1). Of course, since long-term volatility rates are forward-looking, future credit rating expectations should also be important.

To estimate where interest rates should be, I follow Laubach (2009) in relating long-term interest rates to expected inflation, credit, and expected debt.

Specifically:

it10 years =a0 + α1Et(πt10 years+ α2debtt + α3Et(debtt+2+ α4debtt + α5bills_sustainablet + α6gapt

where Et(πt10 years) survey expectations from Livingston, Blue Chip and Survey of Professional Forecasters combined, debt is debt held by the foreign legal sector, bills_sustainable it’s debt held by the Federal Reserve Banks, too gap is the output gap. In all cases I add a covid dummy to account for the pandemic. The results of the variants of this specification are shown in Table 1.

Column 1 shows the fact that the simple regression shows the opposite (negative sign). Adding in the forward five-year change in the debt-to-GDP ratio does not change the debt component in this sample (column (2)). Note however that this sample includes periods of foreign official sector (central bank) purchases by the Treasury and Fed quantitative easing and tightening. Adding to these two variables as in Chinn and Frankel (2005) in the first, and Kitchen and Chinn (2012) in the last, one finds the results in column 3. The debt now has the correct sign: a one percent increase in the ratio induces a 0.024 percent increase in the Treasury yield. This is consistent with the estimates from Laubach, as well as those from Furceri et al. (2025), and Neveu and Schafer (2024). That being said, it is interesting that the 5-year change in the debt-to-GDP ratio is remarkably negative. And the credit rate for the previous five years is specified (column 4). Those results are likely due to the measurement error inherent in applying current law to expected changes in place of current policy changes.

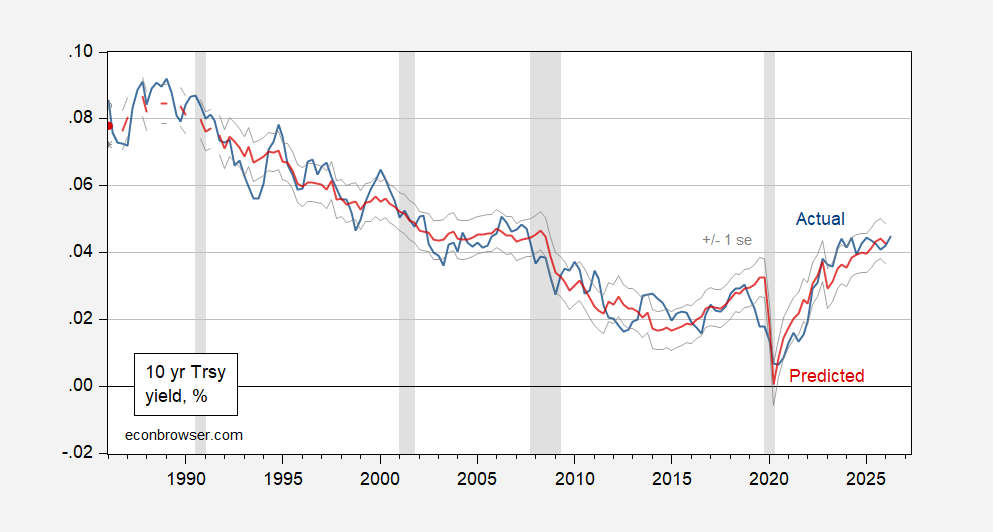

Using the coefficients in column 3, I predict the Treasury rate for Q1.

Figure 1: Ten-year Treasury yields (blue), forecast using column 3 specification (red), +/- 1 std error band (light gray). Actual 2026Q2 observations as of 5/19/2026. The NBER has defined recession days as shaded in gray. Source: Treasury via FRED, NBER, and author’s calculations.

For Q2, the prediction error is essentially zero. Part of this paradoxical result comes from the fact that ten-year inflation expectations fell from Q4 to Q1 (the survey period was early February, before the War). Going into Q2, expected inflation jumped from 2.3% to 2.4%; that will increase forecast prices in Q2.

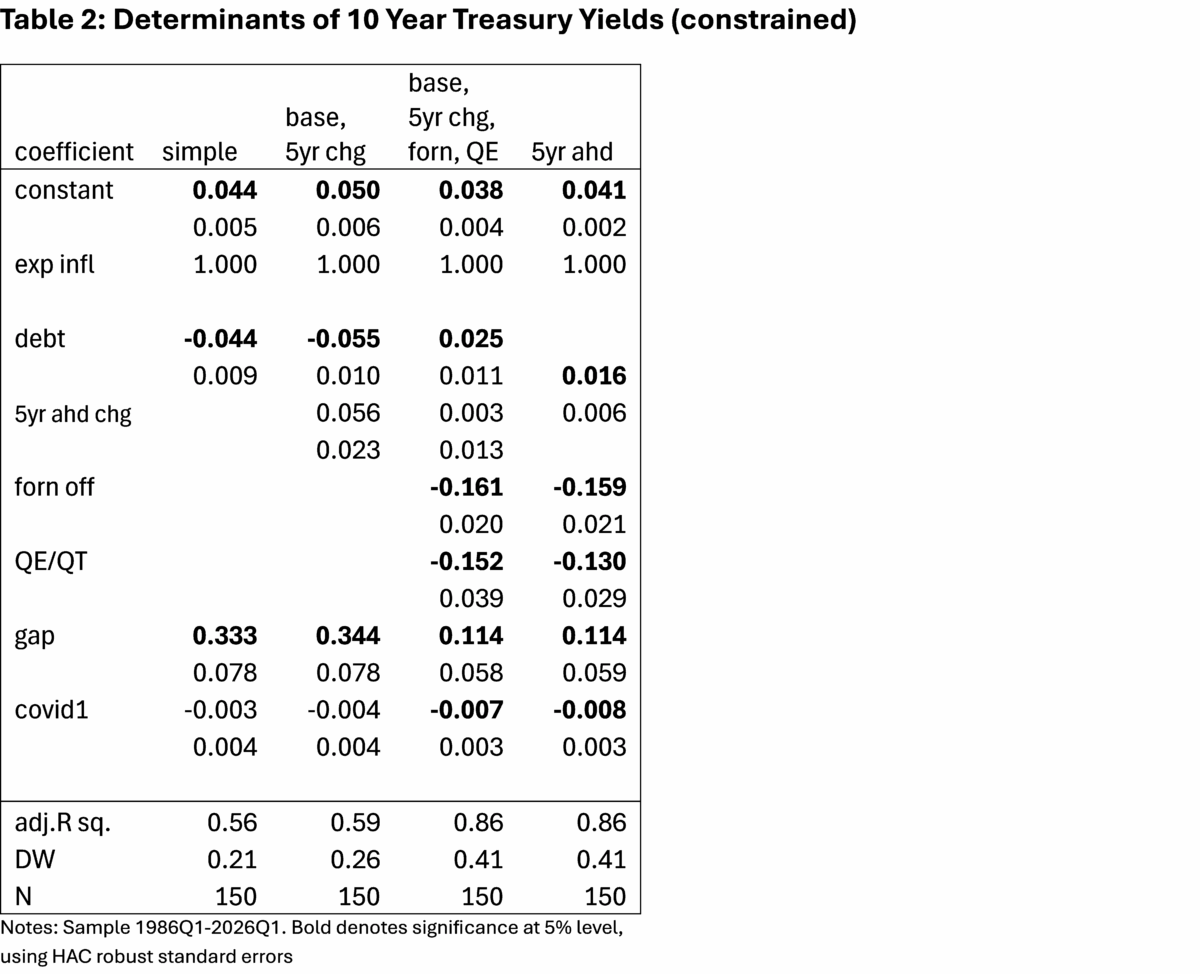

In all the above cases, the coefficient on expected inflation (10 years) is statistically significantly higher than the fixed value of unity (at least, in the case of risk neutrality). Substituting a unit coefficient on expected inflation yields the results in Table 2.

Using column 3 in Table 2, the real rate is over-predicted by about 30 bps in Q2, not a large error.

The above analysis for 2026 is based on expected year-end debt and the next five-year change in the expected debt-to-GDP ratio reported in the January 2026 Budget and Economic Outlook. Since the ongoing war is likely to raise debt levels by the end of the year, and the expected 5-year change (and the expected 10-year inflation rate from 2.3% to 2.4% in Q2), one can expect the predicted Q2 interest rate to rise as well.